Evaluating the Financial Foundation | TPV and Wallet Monetization

To understand how digital wallet monetization is evolving in 2026, we must examine the raw transaction data and the underlying profitability metrics. Comparing PayPal and Block reveals two companies operating at entirely different scales but with vastly different margin structures.

Total Payment Volume (TPV)

PayPal is a global behemoth. Its annual Total Payment Volume consistently exceeds 1.5 trillion dollars, driven by its ubiquitous presence across global e-commerce platforms and its enterprise processing arm, Braintree. Block, formerly known as Square, processes a smaller overall volume, reflecting its concentrated focus on local retail and independent service providers.

Transaction Take Rates

The take rate is the percentage of a transaction the company keeps as revenue. Here, the dynamics shift. PayPal generally operates with a highly competitive but compressing take rate due to its reliance on large enterprise clients who demand volume discounts. Block typically commands a higher net take rate because it provides end to end software, hardware, and point of sale solutions to small and medium businesses that cannot negotiate lower fees.

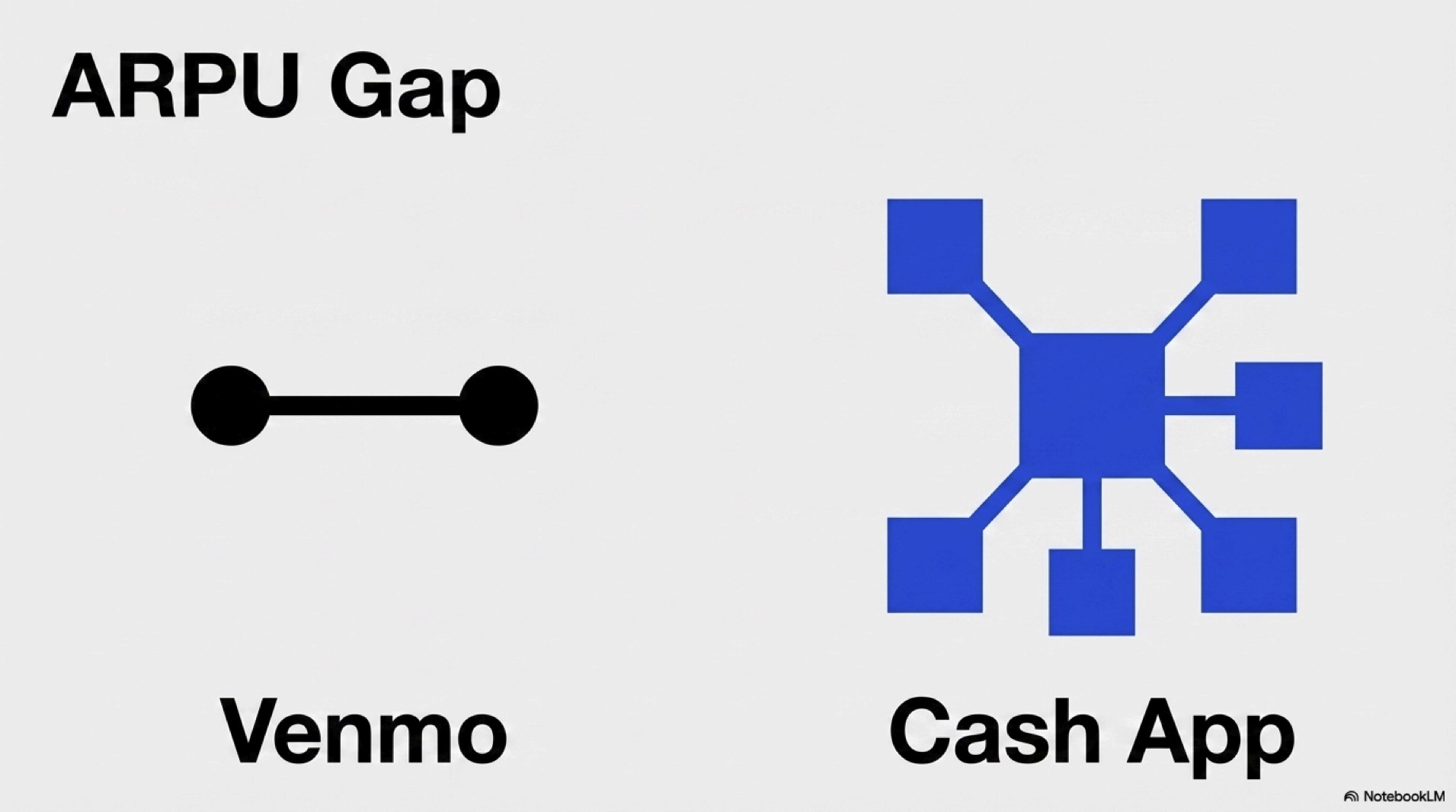

Digital Wallet ARPU (Average Revenue Per User)

When comparing Venmo (PayPal) and Cash App (Block), the monetization gap becomes highly apparent. Venmo boasts massive user numbers but relies heavily on peer to peer transfers, which are notoriously difficult to monetize. Cash App functions more like a digital bank. By integrating direct deposits, stock trading, and Bitcoin transactions, Cash App generates a significantly higher ARPU, successfully turning individual users into highly profitable financial hubs.

Strategic Divergence | Global Checkout vs. Closed Loop Ecosystems

The core difference between PYPL vs SQ stock performance lies in how they construct their merchant relationships.

PayPal operates a highly defensive, horizontal strategy. They want the PayPal or Venmo button on every single digital checkout page on the internet. Their goal is volume and frictionless online payments. By streamlining the online purchasing process and aggressively rolling out innovations like "Fastlane" to optimize guest checkouts for merchants, they capture massive amounts of global consumer data. This makes them an indispensable partner for major retailers, though they rarely interact with the physical storefront.

Block takes an aggressive, vertical approach to build a closed loop ecosystem. They do not just process the payment. They provide the physical point of sale hardware, the inventory management software, and the payroll systems for the small and medium business owner. Furthermore, Block bridges its merchant (Square) and consumer (Cash App) ecosystems through its integration of Afterpay, driving "Buy Now, Pay Later" volume that boosts merchant sales while locking in consumers. Through Square Loans, Block uses real time transaction data to instantly underwrite and issue working capital loans to these businesses. By controlling the consumer side and the merchant side, Block creates a deeply entrenched financial ecosystem that traditional banks cannot replicate.

Macroeconomic Insights | The SMB Lending Market Advantage

As the global economy transitions into a period of slowing inflation, consumer behavior is shifting. When everyday costs stabilize, discretionary spending naturally recovers. People begin visiting local coffee shops, independent boutiques, and neighborhood restaurants with greater frequency.

This macroeconomic environment uniquely favors Block. Because Block is physically embedded in these local storefronts, a surge in discretionary spending immediately translates into higher transaction revenues. Moreover, as these small businesses experience increased foot traffic, they require capital to buy inventory and hire staff. Block seamlessly captures this demand through its SMB lending market operations, securing high margin interest revenue with relatively low default risk, since loan repayments are automatically deducted from daily sales.

PayPal will undeniably benefit from a broader economic recovery as overall online shopping volume increases. It remains the ultimate anchor for stability in the fintech sector. However, for investors tracking fintech stocks in 2026, Block presents a superior structural advantage for capturing deep, value added profitability within the recovering merchant ecosystem.

Disclaimer: All financial data and market projections are based on industry consensus estimates for 2026. This content is provided strictly for informational purposes and should not be construed as personalized financial advice. Investing in financial technology equities involves market risks. Always perform independent research or consult a licensed professional before making capital allocation decisions.