AI in the Operating Room | Evaluating MedTech Moats (ISRG vs. MDT) in 2026

As hospitals face tightening capital expenditure budgets, Intuitive Surgical relies on its massive recurring revenue from procedure volumes, while Medtronic leverages a broad turnkey portfolio to secure its position in the 2026 robotic surgery market.

9

min read

9

min read

The intersection of artificial intelligence and physical healthcare has transformed the modern surgical suite. Driven by an aging global population and persistent shortages in clinical staffing, hospital administrators are aggressively pursuing automation. This necessity has elevated medical technology into a highly lucrative and defensive investment sector. For those tracking healthcare equipment trends, evaluating the economic moats of the dominant players is essential. A comprehensive ISRG vs MDT financial comparison reveals how different corporate strategies are capturing the immense cash flow generated within the robotic surgery space.

The Objective Baseline: Financial Profiles and Market Penetration

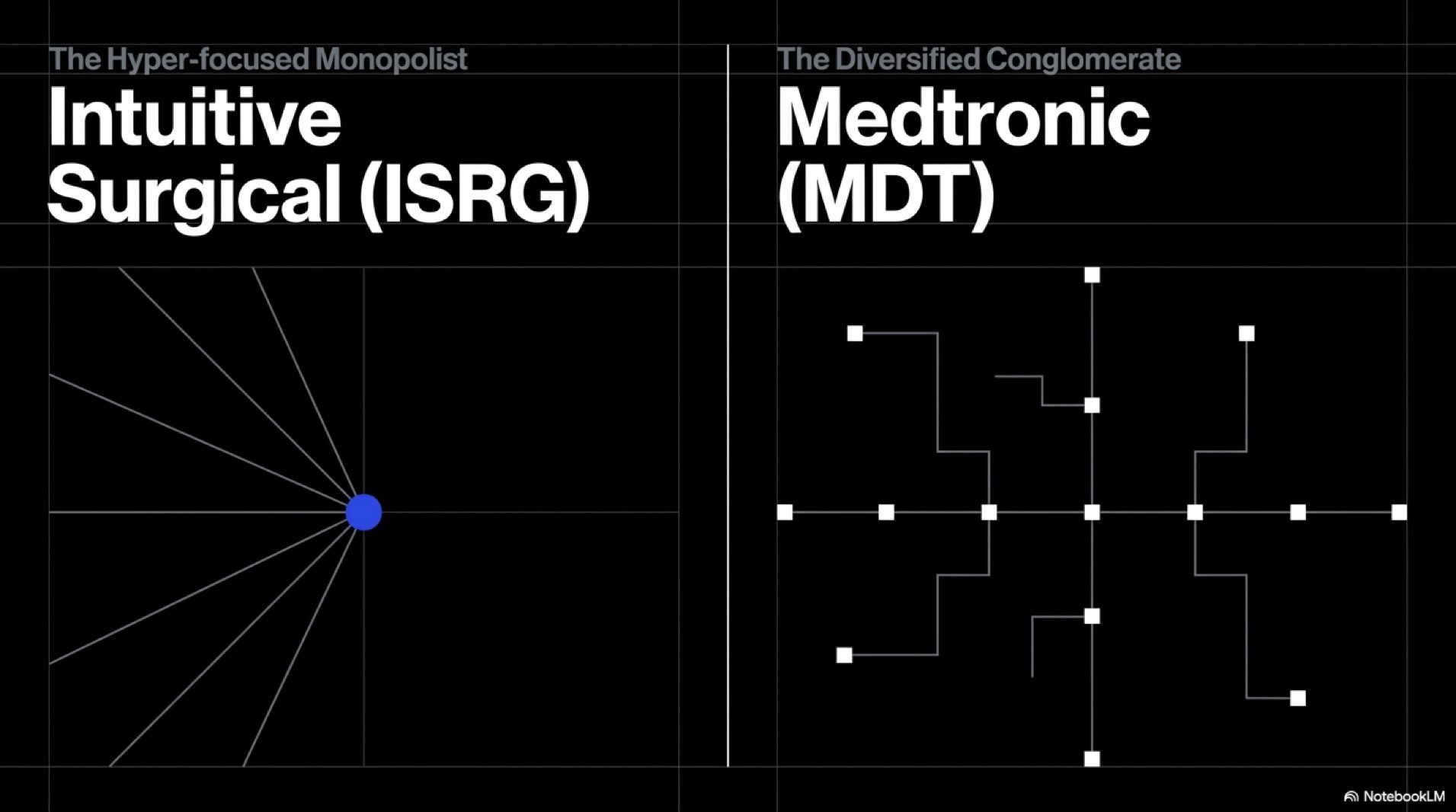

To understand the 2026 MedTech landscape, it is necessary to examine the core financial engines driving 이 organizations. The data highlights a stark contrast between a hyper-focused robotics monopoly and a diversified medical conglomerate.

Core Metric (2026 Industry Consensus)

Intuitive Surgical (ISRG)

Medtronic (MDT)

Global Robotic Installed Base

Exceeding 9,000 Da Vinci Systems

Growing footprint (Hugo RAS and Mazor)

Recurring Revenue Proportion

Approximately 80% to 83%

Roughly 50% to 60% (Varies by division)

Operating Profit Margin

Consistently near 25% to 28%

Stabilizing around 18% to 20%

Primary Surgical Focus

Soft tissue and general surgery

Spine, neuro, cardiovascular, and soft tissue

Business Model Divergence: The Razor and The Hospital Suite

The fundamental difference between 이 robotic surgery stocks in 2026 lies in the paths to profitability.

Intuitive Surgical operates what is arguably the most successful razor and blade business model in modern medicine. The primary product is the Da Vinci surgical robot. However, the initial sale of the machine is merely the beginning of the revenue cycle. Every time a surgeon performs a procedure, specialized, single-use instruments and accessories must be used. This creates a massive, highly predictable stream of MedTech recurring revenue. Because hospitals have already invested millions into training surgical staff exclusively on the Da Vinci system, the switching costs are astronomically high. Furthermore, the rollout of the next-generation Da Vinci 5 (dV5) system, which integrates massive AI computing power and force-feedback technology, solidifies 이 almost impenetrable economic moat for the next decade.

Medtronic approaches the market with a broader, highly defensive turnkey strategy. While competing directly in soft tissue robotics with the Hugo RAS system, the true strength is diversification. Medtronic provides everything from cardiac pacemakers to specialized spinal robots like the Mazor system. Beyond hardware, the company is aggressively expanding the digital ecosystem through AI-driven analytics platforms like Touch Surgery, which integrates seamlessly across devices. When a comprehensive hospital network looks to upgrade an entire surgical department, Medtronic can bundle multiple disciplines and software platforms together. This ability to act as a single, comprehensive vendor gives Medtronic significant leverage and pricing power when negotiating massive enterprise contracts with hospital purchasing directors.

Macroeconomic Insights: Procedure Volume Over Equipment Sales

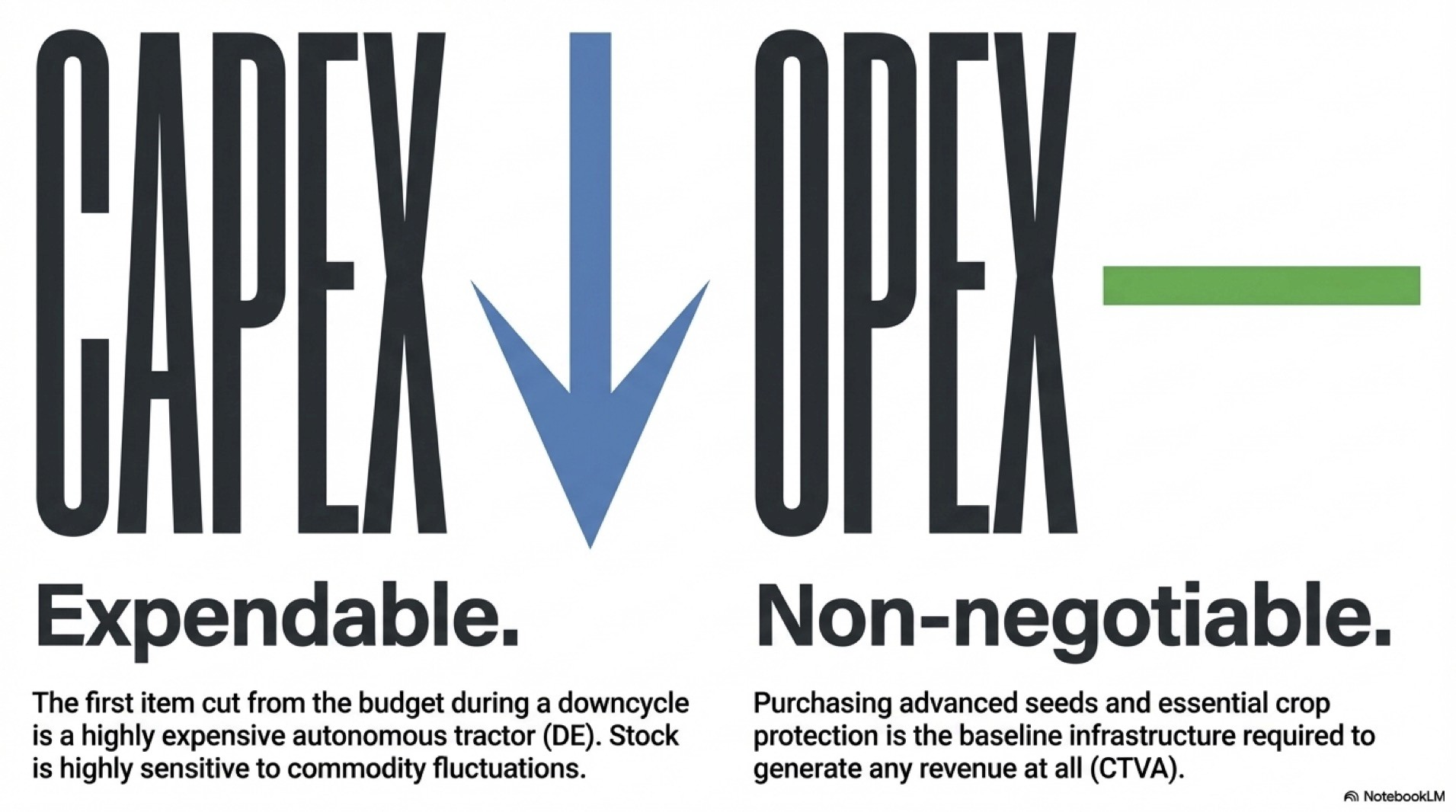

The macroeconomic environment of 2026 dictates a specific strategy for investors looking at the healthcare equipment sector. Currently, hospital systems globally are experiencing compressed profit margins due to rising labor costs and inflation. Consequently, capital expenditure budgets for buying new, multi-million dollar robotic systems are becoming noticeably tighter. Hospital administrators are reluctant to authorize the purchase of new hardware.

In 이 environment, profitability is driven by procedure growth rather than new equipment sales. The ability to monetize the existing installed base becomes the ultimate metric of success.

The Utilization Advantage: Intuitive Surgical thrives in a tight CAPEX environment. Because revenue is overwhelmingly tied to the volume of surgeries performed on existing machines, profits continue to grow as long as patients need operations. Financial health is insulated from hospital budget freezes on new equipment.

The Diversification Buffer: Medtronic faces slightly more friction if hospitals delay buying new spinal or cardiovascular robots. However, the vast portfolio of essential, non-discretionary medical supplies ensures that total revenue remains highly stable, even if the robotics division experiences slower hardware sales.

Ultimately, evaluating MedTech moats requires looking past the shiny AI hardware. The true winners in the 2026 operating room are the companies that can consistently monetize the daily workflow of the surgeon, turning physical medical necessities into compounding financial returns.

Disclaimer: This content is for informational and reference purposes only, not financial advice. Always conduct independent research before investing.