Pricing Power in 2026 | Evaluating Defensive Moats in Waste Management (WM vs RSG)

As economic uncertainties loom in 2026, Waste Management and Republic Services prove their recession-proof resilience by turning regional monopolies and Renewable Natural Gas investments into compounding cash flows.

8

min read

8

min read

Regardless of the macroeconomic climate, one universal truth remains constant. People will always generate trash. This simple reality makes the waste management sector one of the most structurally sound defensive investments in the global equity market. Today, this industry is evolving far beyond basic garbage collection. By transforming landfill methane into Renewable Natural Gas (RNG), these companies are becoming massive players in the ESG energy sector. For institutional investors evaluating recession-proof stocks in 2026, the entire conversation centers around the immense pricing power held by two giants. A deep dive into WM vs RSG financial metrics reveals how these companies protect their margins during economic downturns.

The Objective Data: Margins and Sustainability Investments

To understand the sheer financial strength of these organizations, it is essential to look at their core profitability and how they are allocating capital for the future.

Metric (2026 Consensus Estimates)

Waste Management (WM)

Republic Services (RSG)

Operating EBITDA Margin

Approximately 29% to 30%

Approximately 30%

Core Price Yield

Consistently near 6.5% to 7.0%

Consistently near 6.5% to 7.0%

RNG and Sustainability CAPEX

Exceeding 1.2 Billion Dollars

Expanding aggressively via joint ventures

Both companies operate with incredible efficiency, boasting EBITDA margins that rival top-tier software companies. Their Core Price Yield, which measures their ability to raise prices on existing customers, remains consistently strong. However, their capital allocation strategies reveal slightly different long-term priorities.

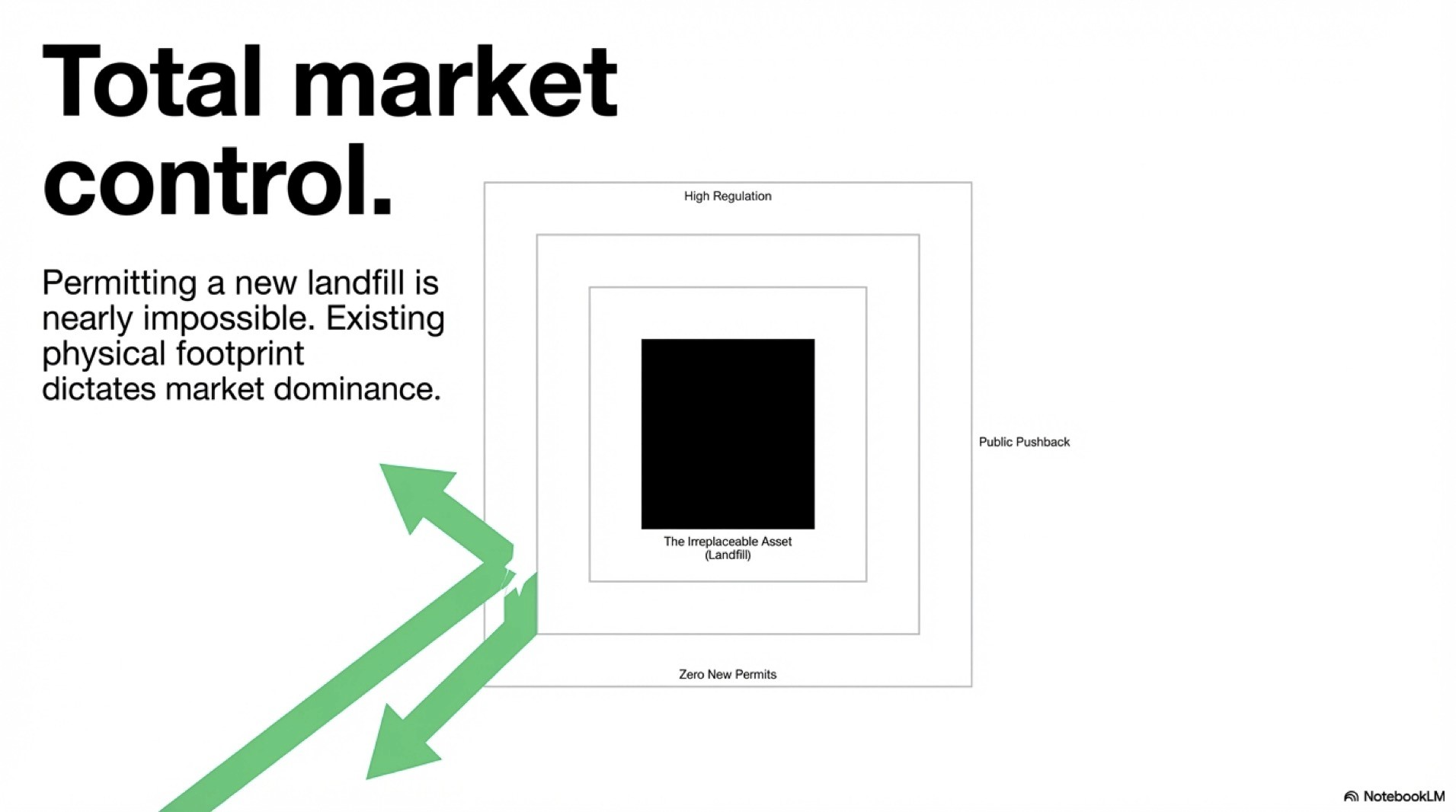

Evaluating the Moats: Landfill Dominance vs. M&A Rollups

The economic moat in the waste industry is arguably the strongest in the physical world. Permitting a new landfill is nearly impossible due to local regulations and public pushback. Therefore, the companies that already own the holes in the ground control the entire market.

Waste Management (WM) and Technological Scale

WM is the undisputed heavyweight champion of landfill ownership. Their strategy relies on leveraging this massive, irreplaceable physical footprint. To maximize profitability, WM is aggressively investing in robotic sorting and optical scanners at their recycling facilities. By automating the sorting process, they drastically reduce their reliance on human labor, structurally lowering their operating costs. Furthermore, WM is deploying massive capital into Renewable Natural Gas (RNG) investments, building facilities that capture landfill methane and sell it directly into the national pipeline grid as premium-priced green energy, while simultaneously capturing highly lucrative Renewable Identification Number (RIN) environmental credits from the EPA.

Republic Services (RSG) and the Roll-Up Strategy

Republic Services operates with a highly focused, localized approach. While they also own a massive network of landfills, their growth engine is heavily fueled by strategic Mergers and Acquisitions. RSG excels at the "roll-up" strategy. They identify highly profitable, independent regional waste collectors, acquire them, and integrate them into the broader RSG network. This allows them to quickly dominate secondary and tertiary markets, creating unbreakable local monopolies. In the RNG space, RSG often utilizes joint ventures—most notably their massive partnership with BP’s Archaea Energy—allowing them to capture the ESG upside while sharing the upfront capital expenditure risks with established energy partners.

The Ultimate Inflation Hedge and Recession-Proof Asset

The defining characteristic of a true recession-proof stock is the ability to pass costs directly to the consumer without losing market share. This is known as pricing power.

During inflationary periods, fuel costs and labor wages spike. Waste management companies are uniquely insulated against this threat. The vast majority of their revenue comes from long-term municipal and commercial contracts. These contracts are specifically written with built-in inflation escalators, often tied directly to the Consumer Price Index (CPI). When inflation rises, WM and RSG automatically raise their collection fees. The consumer pays the higher price because trash collection is a non-negotiable, essential service.

As we navigate 2026, the transition of landfills from simple waste repositories into active, green energy-producing assets changes the valuation models completely. By successfully turning an environmental liability like methane gas into a highly lucrative revenue stream, both Waste Management and Republic Services have cemented their status as the ultimate defensive anchors for any long-term portfolio.

Disclaimer: This content is for informational and reference purposes only. Always conduct independent research before making investment decisions.