Pricing Climate Risk | Progressive (PGR) vs. Chubb (CB) in the 2026 Insurance Macro

While Progressive leverages AI telematics to aggressively price retail auto policies and protect margins, Chubb utilizes its massive global commercial portfolio to absorb escalating climate risks and secure steady corporate cash flows.

9

min read

9

min read

The property and casualty insurance sector is experiencing a profound technological and environmental transformation. The frequency of catastrophic weather events is colliding with massive inflation in vehicle and property repair costs. This volatile environment has made AI in insurance underwriting the defining factor for corporate survival and profitability. For investors evaluating P&C insurance stocks in 2026, the market presents two highly successful but fundamentally different approaches to managing these climate risk macro trends. A detailed PGR vs CB stock comparison reveals how distinct data strategies generate massive, predictable cash flows.

Objective Financial Benchmarks and Profitability

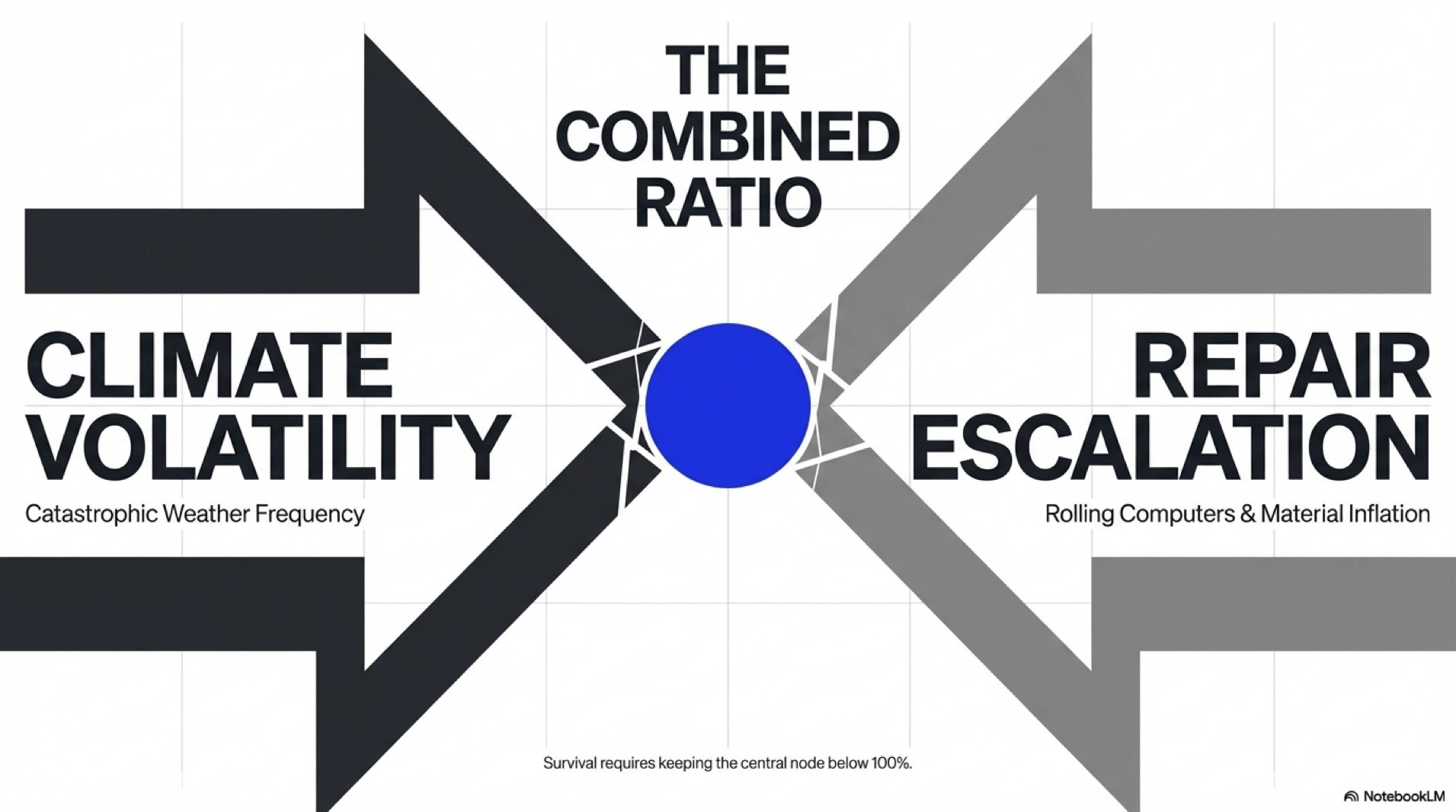

In the insurance industry, the ultimate metric of operational health is the Combined Ratio. A ratio below 100 percent means the company is generating an underwriting profit before even investing its premium float. Examining the current financial landscape shows two exceptionally well-managed entities.

Metric (2026 Consensus Estimates)

Progressive (PGR)

Chubb (CB)

Combined Ratio

Exceptionally low (Typically 88% to 91%)

Highly stable (Typically 86% to 89%)

Net Premiums Written Growth

Aggressive double digits (15% to 20%)

Steady and predictable (8% to 11%)

Return on Equity (ROE)

Roughly 25% to 28%

Roughly 14% to 16%

Both companies operate well below the 100 percent threshold, making them highly profitable. However, their pathways to achieving these elite margins rely on entirely different customer bases and risk models.

AI Telematics versus Global Commercial Diversification

The core difference between Progressive and Chubb lies in how they underwrite risk and who they choose to insure.

Progressive is the undisputed king of retail auto insurance and data analytics. They pioneered the use of telematics through their "Snapshot" program, plugging devices into cars and using smartphone apps to track exact driving behaviors. Progressive uses advanced AI models to process this granular data, allowing them to price policies with surgical precision. If a customer is a high-risk driver, the AI immediately flags it and raises the premium or drops the coverage. This hyper-responsive model allows Progressive to maintain incredible profit margins even when the broader auto market is struggling with rising accident severities.

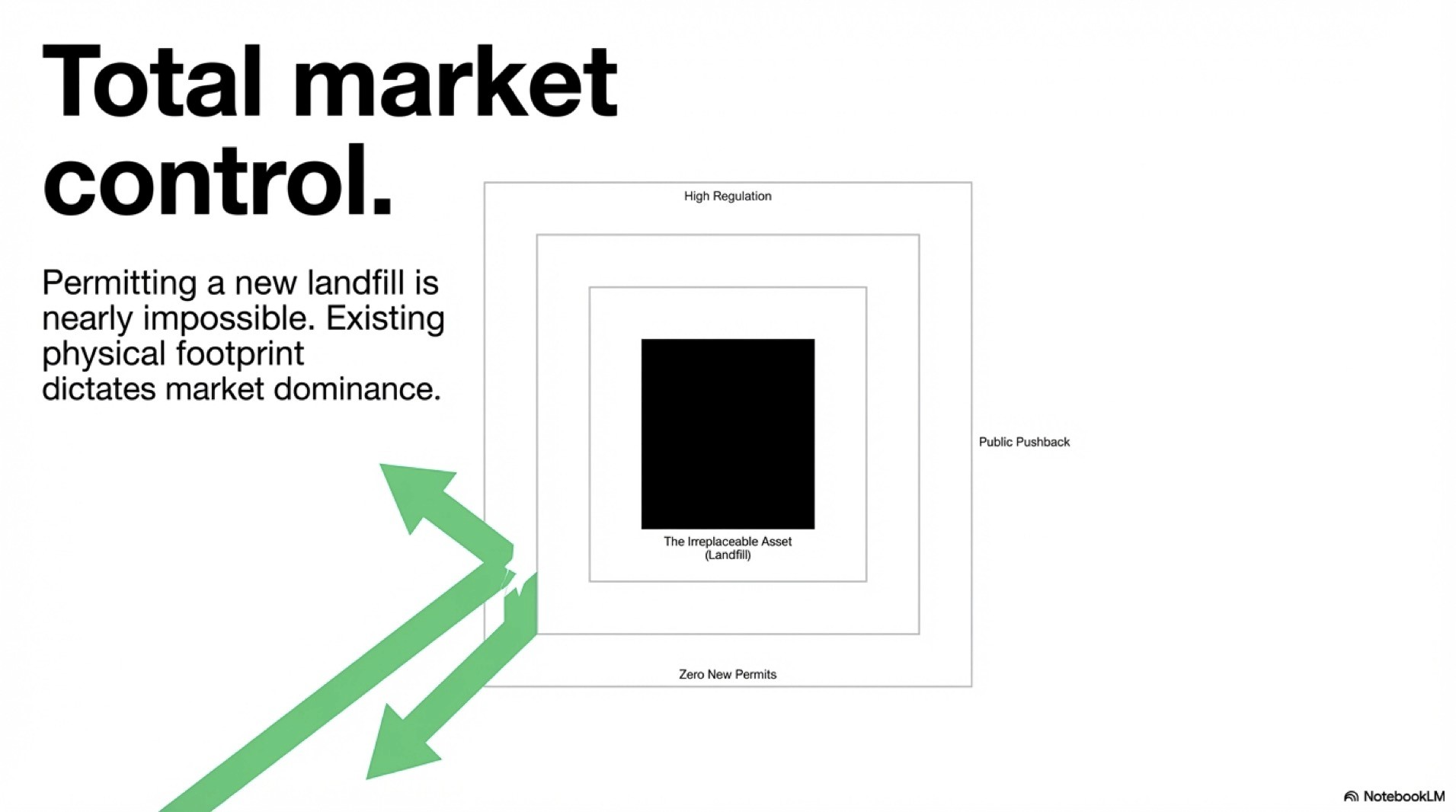

Chubb operates on a completely different scale. While they offer standard personal lines, their true strength is in commercial insurance and serving ultra-high-net-worth individuals through their renowned "Masterpiece" policies. They underwrite complex, massive risks for multinational corporations. When dealing with climate risk macro trends, Chubb relies on geographic and product diversification. A severe hurricane in Florida might trigger significant payouts, but Chubb offsets those losses through highly profitable corporate liability policies written in Europe or Asia. Furthermore, their high-net-worth property policies often include proactive climate defenses, such as deploying private firefighting units, which drastically mitigates total loss. Their defense against climate volatility is pure, unadulterated global scale.

Inflation, Pricing Power, and Margin Protection

The defining challenge for the 2026 insurance market is the persistent inflation in repair costs. Modern cars are essentially rolling computers, and repairing them after a minor fender bender costs significantly more than it did a decade ago. Similarly, rebuilding homes after a storm involves elevated labor and material expenses.

In this environment, Pricing Power is everything. If an insurer cannot pass these rising costs onto the consumer, their combined ratio will quickly spike above 100 percent.

Progressive demonstrates absolute dominance in pricing power within the retail space. Because their AI models detect rising claim costs in real-time, Progressive files for rate increases with state regulators months faster than their legacy competitors. By the time inflation impacts the broader market, Progressive has already adjusted its premiums to protect its profit margins.

Chubb holds massive pricing power in the corporate sector. Global enterprises require specialized coverage for complex supply chains and cyber risks. There are very few insurers globally with the balance sheet capacity to underwrite these massive policies. This lack of competition allows Chubb to consistently raise premiums on corporate clients without losing significant market share, creating a fortress of steady, high-quality cash flow.

For investors, Progressive offers an aggressive, technology-driven growth engine optimized for the retail consumer. Chubb provides a globally diversified, high-net-worth anchor that acts as a premier defensive asset against broader macroeconomic shocks.

Disclaimer: This content is for informational and reference purposes only. Always conduct independent research before making investment decisions.